Micron Investment Thesis

Micron (MU) is widely regarded as one of the best firms to produce memory for AI chips with their DRAM and HBM mix. MU has been on a tear here lately mainly due to the increase in data centers and the current state of AI speculation. Data centers are popping up left and right with a demand for more and more energy.

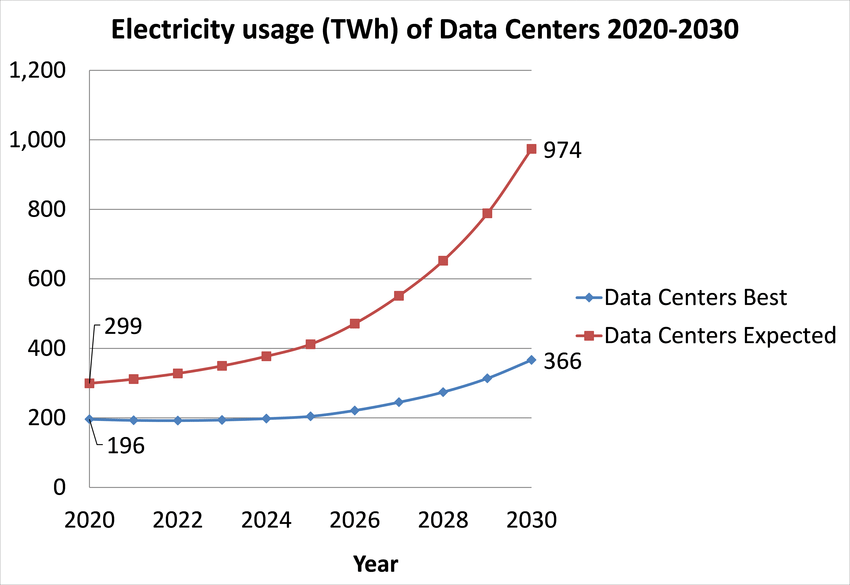

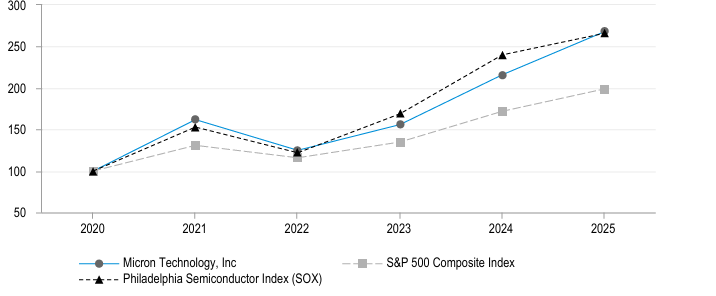

Above we can see two lines which display the current power of data centers we have now compared to high powered AI data centers that we will need. Looking forward we can see that in 2030 it is estimated that the power of these data centers will be triple what we will have if we remain constant. Currently in 2026 our highest power data center is running around 180 TWh which is not even close to the estimated 974 TWh we are projected to need. Data centers rely heavily on companies like MU to produce the memory for the data centers. Essentially, they are selling shovels in a gold rush as their DRAM and HBM are integral in the data centers functionality. Micron has significantly outperformed the S and P and majority of the broader indices which in itself is impressive but not a sole investment driving decision.

MU has a heavy presence in the US, Asia, and Europe which is a good indicator but when looking at the threat of systematic rick in the broader market. MU currently has a β of 1.50 rising from a 1.15 in 2022. MU β presents a Δ of .35 which signals that MU is more volatile than the market in itself so for a more risk averse investor this may not be a good investment. MU EPS has constantly rose Q/Q but we also see a massive jump in underlying stock price which would indicate a higher forward valuation. Forward valuations are basically the expected future results of the company put into the current value of the underlying spot price which indicates heavy market expectations for MU but if they are not met and AI data center demand is not still driving then this could hurt MU. Data center demand comes with many what ifs such as the one stated earlier in the sense of will we be able to sustain the energy level needed to actually optimize AI or will we become stagnant in the AI race. No matter your view on AI even if it is bearish we can all agree that the future expectations on these data centers are insane. MU is shining from this, but will it hold?

Where is the money?

My guide to MU

MU as stated above is very volatile and is on a tear. MU can look like a solid investment (which it could be) but with a good grasp on what is going on. Options on MU would be very risky as it moves a significant amount either way very frequently and even selling them wouldn't be a good idea (writing puts with a bullish outlook maybe). IV is extremely high for a stock moving at this pace so any flat spans would destroy your contracts and would bring the value down. Q/Q revenue in quarter 1 2026 was 2.80 X relative to 2024 which is very impressive. Equity in the company is my current strategy as I believe the demand will still grow and they will be the supply which is a very bullish indicator in my eyes. Other than data center exposure. MU is the third largest DRAM manufacturer with a 15% share in the market (Samsung 45%, SK Hynix 20%) with these being said MU is the largest domestic DRAM manufacturer as the top two are Korean companies. With 80% of the market being controlled by three big firms we can see the pricing power for MU is pretty strong especially in the AI race as the companies are racing for the best AI and this can increase MUs leverage when it comes to terms. Pricing power is very integrated in the supply and demand cycle as well so if the demand moves down and the supply stays the same, we will see a massive decline in revenue as the market will be diluted with unwanted products which could easily water down the price. Demand decreasing to this point would require a complete outlook shift in the future of tech as this would also mean data center expansion would slow and other tech firms will take a hit also.

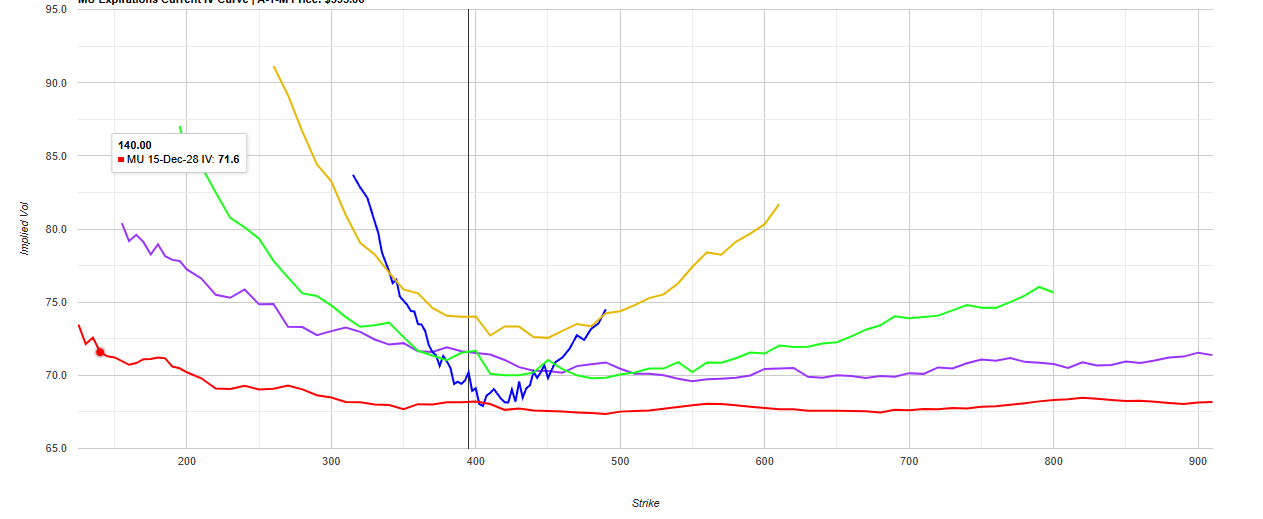

Above we see the IV of contracts ranging all the way to 15-Dec-28(very bottom line). IV is constantly near the 70 mark which is pretty high especially for a cyclical industry like MU is in so one downturn and the IV is coming down. Options for hedging would be a great idea here especially to pay the raised IV premium to protect you from a vicious downturn because the expected return is so high if it grows that premium will not hurt your gains that much. Puts at a comfortable selling price long dated would be ideal, in case this hype runs out you will at least be covered to some extent. Long strangles could also be a smart move as MU rarely trades flat giving you the ability to push your wings to maximize potential profit.

Above we see the option strategy- Long strangle which consists of you buying OTM calls and puts which is going against my options claim earlier (Not really). MU is not a stock you want to take a directional bet on but with the strangle you get exposure to both ways with the loss stemming from a flat trendline which MU does not know what that is at this current time. Strangle or equity is a preference if you think the demand will stay then you can profit from both or if you are bearish on the demand but still want upside exposure the strangle is for you. Overall I would say MU is a solid buy with many bullish traits but as you start buying MU it is very important to know the industry cyclical nature and prepare whether that's options, stop losses, or not buying it is up to you but a downturn is very possible but short term turbulence happens to every company.

Market thoughts

My current ideas and thoughts

Software companies took a massive hit early in 2026 with the beast of an AI company in Anthropic coming out showing their AI can replace a lot of the software companies. Hedge funds have been making a lot of money shorting the smaller software companies that will be replaced by AI in the future and recently Anthropic showed that the AI takeover is definitely relevant as the market reacted heavily. OpenAI is still under fire, and many large companies are pulling their initial investment back as the concern for their revenue is still up in the air as they are missing what Anthropic has at least to me. Software companies such as Palantir (PLTR) will be an interesting watch as their revenue streams heavily from government work so a decline from this reason would mean the government is putting serious work in AIs hands. PLTR was one of the biggest reactors to this mini software crash as that makes me question can AI automate warfare tactics? Anthropic right now is currently on the mission to automate "grunt work" in large banks but can we see the future of AI shift more towards the war front especially replacing the human. AI is already used pretty heavy when it comes to tracking and drones. AI has already changed the job market a lot but with new AI replacing software comes loss of jobs in a specialized field which will cause high wage pressures as they are making very good money working in software. SAAS companies will see an influx from the smaller companies that got replaced leaving a majority of people without a job and a waste of human capital but at the cost of AI being cheaper. Where will these smaller software workers rotate to? Will AI replace all software? Ethical AI guidelines? these are some of my questions, but my biggest concern is the pace at which AI is moving every time you look up there is a new AI version or a new job being replaced by this overarching power that we built. AI hype is insane and it makes you wonder how much of that hype is real vs. highly unrealistic expectations.

Chipotle (CMG) has been very strong and my original piece https://www.the-green-candle.com/chipotle-investment-thesis/ has been very strong and correct. CMG is still on my radar as selling CCs on them is a very profitable strategy and the rapid small-town development is still in full swing.

I will likely write about the scam, or I mean company named MicroStrategy and where exactly I stand on them. MSTR is a very different company as their underlying performance is related to a non-backed cryptocurrency. Something to think about could be as follows will MSTR ever be liquidated and what is the overall market effect of a serious Bitcoin crash?

Thanks for your time!