Sneaky alpha: CAT Bonds

Portfolios are usually at risk for one big thing and that is systematic risk which can destroy the whole market essentially. Portfolios consisting of mainly equities will not be " Diversified" from market risk in a net positive way usually. As of the time I am writing this we are in full swing of market risk with the Iran situation and repricing from the SAASpocalypse which has most likely brought your portfolio into the red not unless you had short exposure. Market risk can be somewhat avoided by finding uncorrelated returns such as CAT bonds to generate alpha and avoid market risk but rather take on event risk. Diversifying risk is a smart idea, if possible, such as having some of your portfolio exposed to market risk or event risk. Before we get into CAT bonds, I think the term alpha should be looked at in depth. Alpha or α=Ri−[Rf+β(Rm−Rf)], basically actual - expected return. Alpha is how much you beat a benchmark by. Example Stock ABC performs with a solid 10% gain actively in which the CAPM (go to Sharpe ratio paper) model expected a 7% return on the stock we can assume a 3% alpha. Now that we get the idea of alpha let's talk about the center point of this article and that is this weird investment tool being CAT bonds. Debt has this relationship with time being the longer the riskier with all else equal a 30-year bond will be riskier than a 1-year bond. Basic debt knowledge will not be covered here as CAT bonds differ pretty heavy than your Gov, Muni, and corporate bonds. CAT bonds are bonds issued by insurance companies (3-5 years) to help raise capital and transfer risk to investors in which the investor takes on event risk. Event risk on a CAT would be an insurance company worried about a tornado coming through, so they issue CATs to raise capital in case of the emergency. Events with a high probability will bring out bonds with higher yields (Traded at discount so yield is higher) in which the investor can buy the bond and receive interest/coupons. Two things can happen here with the tornado example let's see both. Option 1 the tornado does not come through so the investor would make all the interest plus the face value difference (assuming discount) and will walk away safe while essentially selling insurance for the tornado. Option 2 the tornado comes through and wrecks the town meaning the investor has now lost his investment as this money will now go towards the disaster instead of the investor.

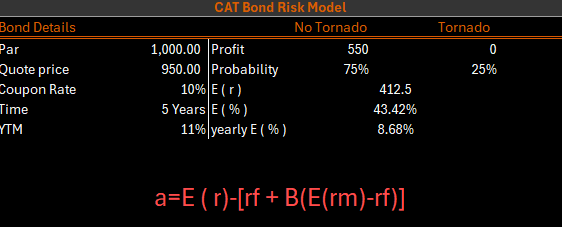

Above I have put a simple model showing the expected return on one CAT bond over the span of 5 years. 43% overall is pretty solid in the made-up example but this is realistic as CAT bonds carry a significant amount of risk (hints the return %). CATs could be smart if the market risk is pretty high and you are bullish on a safe environment where others are not weather wise. Expecting to make a return this high from every CAT is insane but adding them to your portfolio can help take away some of that market volatility that we see so much in today's market. Buying CATs are usually traded OTC which means you can usually only get them from the insurance firm directly or maybe from someone else in a very niche secondary market. CATs being OTC does have some risk in itself as bondholders on CATs usually don't look to sell rather hold till maturity so adding these to your portfolio would also bring in liquidity risk on the debt which if you are bullish on the weather then this is not an issue. Smaller secondary markets also have very little price discovery so finding an actual price on the bond to value it will be relatively hard when looking at something listed on NYSE which has pretty high price discovery. Overall CATs are something to think about and even at a fundamental level they are very interesting as the risk transfer takes place, but you are essentially making money on the weather which can always be intriguing.

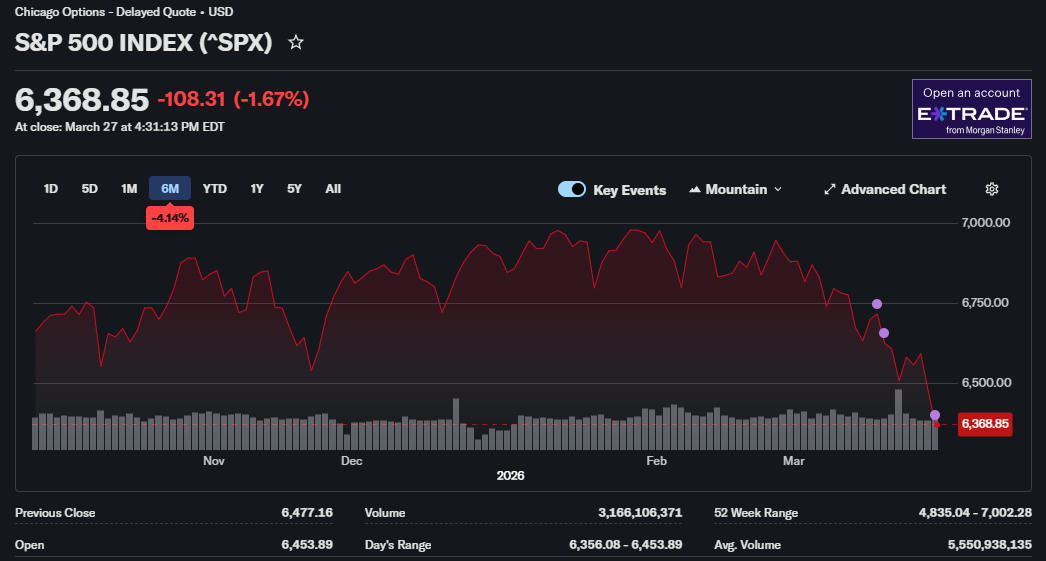

Currently as of 3/28/2026 I believe this would be a good time to start buying as this market correction has been huge and as we can see a VIX above 30 is always pretty scary but long term this could be a very good buying opportunity. Shares are what I would advise here and maybe some options but long dated options as bearish volume has been really strong here lately so your IV will already be pretty high making you bank on a larger move vs. owning shares. Shares in this market will allow you to get a hefty discount on just about anything you are bullish on which could be a good thing if they are included in the recovery or could be bad if they are going through a repricing event. CATs is also another good idea for a market like this as you will be further from the 30 VIX and the blood red SPX instead you will be watching for Tornados, Tsunamis, Hurricanes, etc. which could be a safer game at this point. Understanding the balance between debt and equity in a portfolio is very hard especially what kind of equity and same with debt but at the end of the day having b0oth is always nice and can lead you down a safe street. Noting CATs are not the safest debt as that would be the T-Bill in essence but the idea is not for you to only buy CATs but to realize debt is out there on many things not just large firms like your local school or park was probably built using Muni bonds to some extent. Debt is all around us and it is important to use that to your advantage as a chance to diverisfy away from equities and market risk.